I Grew My Kiwisaver by 24% (over $27k) in 2023

Let me start by saying this isn’t financial advice. It’s simply a statement of what I did to grow my Kiwisaver by $27,000 (from $113,183 to $140,391) in 2023.

And why despite this I am actually looking to move Kiwisaver providers in 2024.

24% Growth in 1 year – an increase of $27,000

Of course a 24% increase sounds impressive, but the truth is that Kiwisaver has been the easiest way to grow my wealth I’ve ever found – joining was simple and now a % of my wages is automatically deducted from every pay before it even makes it to my bank account.

So I don’t have to do anything each payday or month.

There’s no thinking or action required.

And most importantly I can’t be tempted to spend it.

Nor can I withdraw it (except under exceptional circumstances) – until retirement age that is.

I think some people are under the misguided impression that this means the government has my money.

It doesn’t. It’s still my money – and if I were to die before retirement it becomes a part of my estate left to my beneficiaries (my parents, a future partner, or whoever I choose)

Investing in Kiwisaver simply means it is kept safely away from my spendy little hands. Because the government knows me better than I know myself. I might think that I would be disciplined enough to resist touching it until I am 65, but….

The truth is it would be all too easy to be tempted to upgrade my kitchen (and get rid of its ugly green countertop), or to treat myself to that holiday in Bali that is too good a deal to miss, or a new car if my current one died or a pair of the latest season’s fabulous, chunky soled sandals from Merchant….

Investing in Kiwisaver takes those temptations away and ensures that I am saving for retirement.

How I grew my Kiwisaver by $27k in 2023

I’ve been investing in Kiwisaver since I became eligible (when I became a permanent resident) in 2013 – so 2023 also marked 10 years.

But there was a lengthy period when I was self employed that I was only investing the minimum to get the government contribution (the government will contribute 50c for every dollar you invest in Kiwisaver up to $1042.86 – so the maximum they will contribute $521.43) which means I don’t have as much in my Kiwisaver as I should, or as much as I would like.

Still 2023 was a good year.

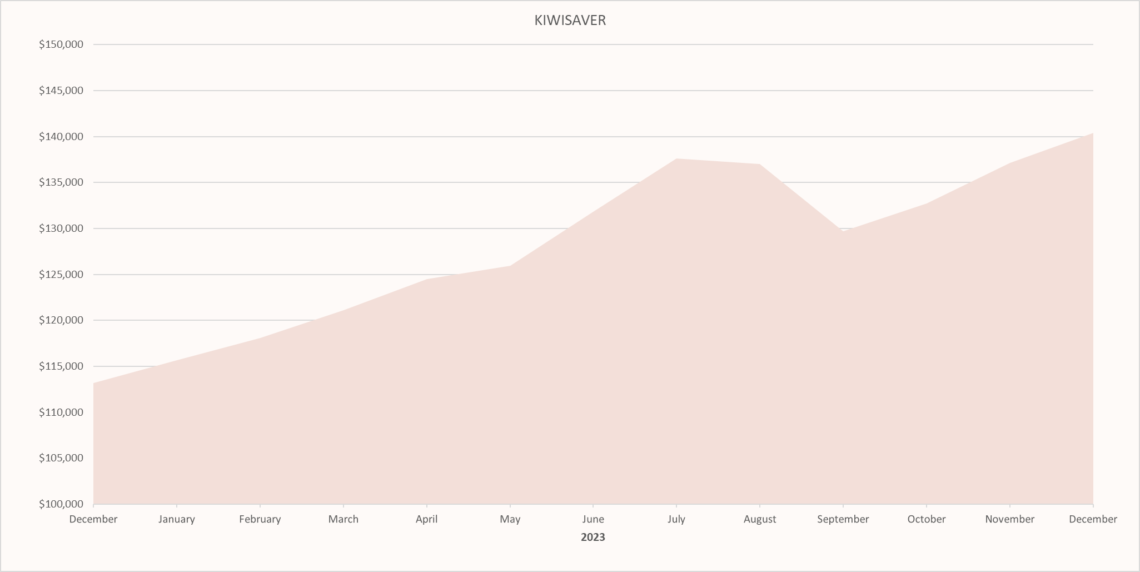

At the start of the year I had a balance of $113,184.

By the end of 2023 this had grown to $140,391.

That’s a 24% increase, which is pretty impressive.

So how did I grow my Kiwisaver by $27,000 in just 1 year?

- I increased my payroll deduction from 3% to 4%

I started a new job in January which came with a small pay increase. So rather than risk that pay increase ending up spent, I took the opportunity to increase my Kiwisaver contribution by 1%. Something I intend to do again any time I get a payrise.

This meant that my contributions as an employee increased from $2,339 in 2022 to $3,528 in 2023.

And with my pay rise my employer contributions also increased from $1,574 to $1,884

(I also have a legacy voluntary contribution of $42 a fortnight from when I was self employed, which I have just never bothered cancelling. But that stayed the same.)

So in total contributions increased by $1,239, which leaves a balance of $25,761.

2. I moved my investments from a conservative fund to more aggressive funds.

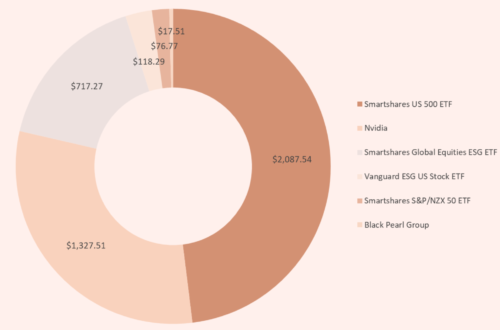

I currently have my Kiwisaver with Booster across 3 funds.

I have a Kiwisaver and a Supersaver scheme where I have the remnants of my UK pension, still held in GBP.

Now my Kiwisaver is invested 75% in the Socially Responsible High Growth and 25% in the Socially Responsible Geared Growth.

My superscheme is 100% in Sterling International Shares which has 100% in MSCI World Index UCITS ETF.

Both are considered aggressive funds. But for the first 5 months of the year my investments were in more conservative funds – until I learned that however worried I am about losing money, I am losing more money by being conservative when I don’t need to be.

3. I sat back and let the stock markets do the rest.

That’s right. Apart from switch funds mid year I did nothing. Just allowing the contributions and stock markets to do its thing.

So the truth is I can’t take much credit for the $27k growth (just $1,239 of credit in fact).

Maybe the change in funds helped. I made the switch in May and by the end of June my Kiwisaver was up over $11k.

But maybe it didn’t because the following month it dropped $576 and by September my balance was lower than June.

Truth be told it is almost impossible (from the information Booster provides at least) to calculate how much of the growth achieved in the second half of the year was through fund choice and how much of it was just from a stonking stock market!

(as I mentioned in my investing post, the S&P 500 returned a whopping 24% in 2023)

So I think actually the most important things I have done with regards to Kiwisaver are in fact to simply:

- Join

- Contribute as much as I can – at least enough to get the Government contribution and my employer match.

- Choose a fund that aligns with my investment strategy – with another 20 years until retirement I can afford to be as aggressive as possible. It will make for a bumpy ride but over that kind of time period it should get me the best returns.

What Now for 2024

So what was that about wanting to change Kiwisaver funds again? Even after a 24% increase??

Yep. And here’s why.

Fees.

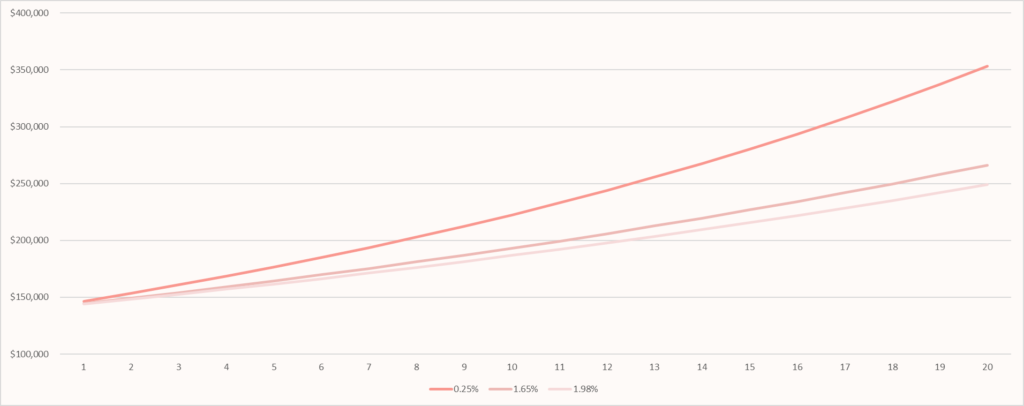

From what I discovered on Sorted’s website (via a recent email from The Happy Saver – thanks Ruth!) Booster has some of the highest fees at 1.65% and 1.98% for the 2 funds I am invested in.

Meanwhile someone like Simplicity offers Kiwisaver funds with fees of just 0.25% (from 1 February 2024)

A 1.73% variance might not sound like a lot. But the compounding effect of that small difference in fees over the course of an investment lifetime can mean $$$,$$$s! (nope, not an exaggeration)

I did some maths (you can take the girl out of the accountants office, but….)

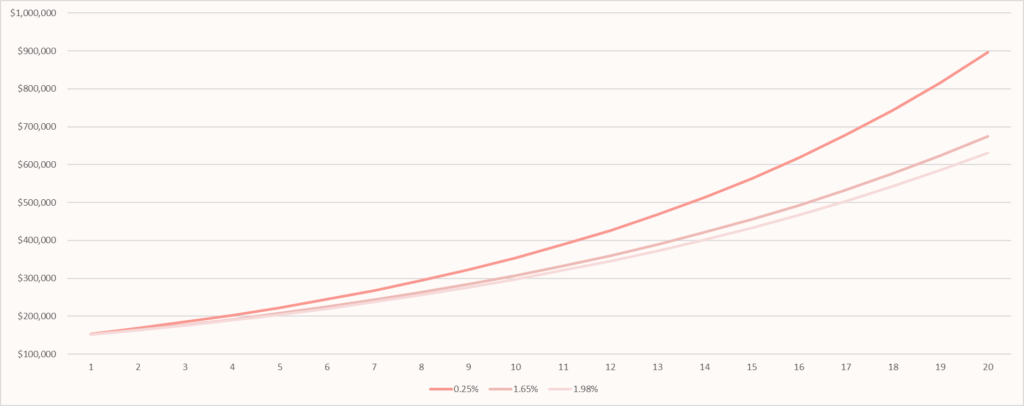

So, if I was to take my $140,000 and for the next 20 years until I retire leave it in the funds they are currently invested in (for simplicity’s sake I have assumed making no further contributions of any kind) I will have (using the 1.98% fees) $249,005 when I retire.

If on the other hand I move that $140,000 to Simplicity where the fees would be 0.25%, I will have $353,323. That’s $104,318 more!

The above is based on a 5% return – which is probably quite conservative as the S&P 500 on average returns about 10% a year over a 10 to 20 year period. Based on 10% the difference is even a bigger – a whopping $264,501.

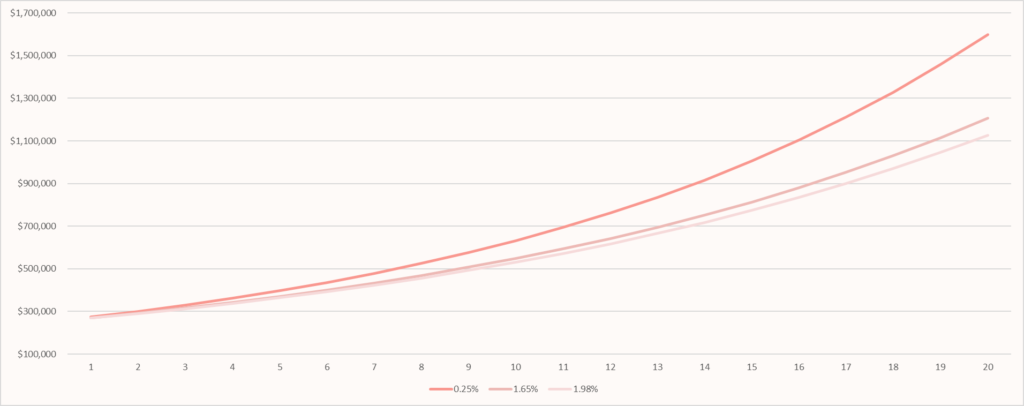

And if I change the investment from $140,000 to $250,000, which someone my age (someone who hadn’t taken a 6 year break from Kiwisaver and didn’t have the disasters I had with my early pension schemes) could easily have, then the difference at retirement between a fund that charges 0.25% and one that charges 1.98% is $186,283.

And increase that return on $250k from 5% to a more realistic 10% and that difference increases to a massive $472,324! Paying fees of 1.98% I would have $1,127,425 and I would probably be quite happy with that. Until I realised that had I invested with a fund that only charged me 0.25% I would have $1,599,749 instead.

Almost half a million dollars more.

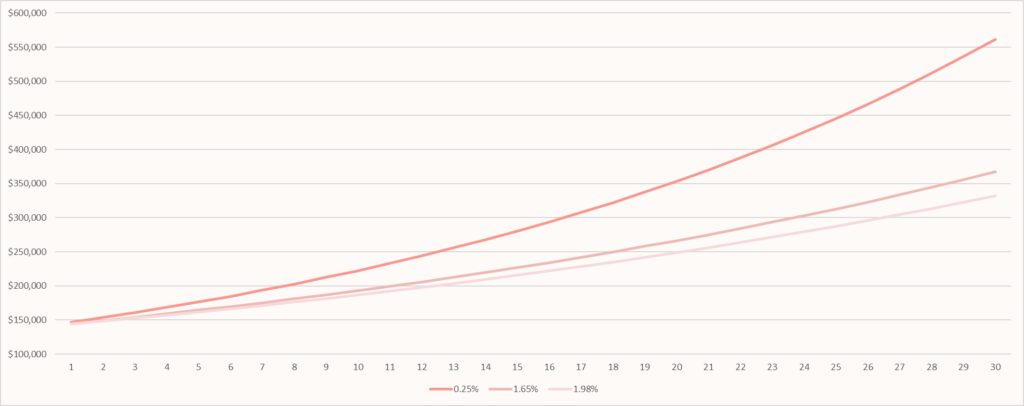

And if I had had $140k at 35 (which if I had started at 20 would have been completely plausible) then the difference in funds after 30 years is ridiculous – even at a 5% return. 0.25% fees would give me $561,299 but with 1.98% fees I would have just $332,084 at retirement – a difference of $229,215.

Yes… I think I will be moving to Simplicity.

Just to end this post I will say, as of today (the 24th of January) my Kiwisaver has increased by another $5k.

Not bad for just over 3 weeks (2 pays)

Amy

XO$