I Cut My Expenses By $23,881 In 2023

I had no idea I had managed to cut my expenses by so much, or even that it was possible I could. Since separating from my husband I thought I had been living frugally – when you are paying a mortgage on a single salary frugality is forced upon you.

No Ubereats, takeaways, wine in my groceries or designer labels for me.

The really weird thing is, 2023 is the first year since 2013 that I flew home… and I had an overseas holiday (to Vanuatu) and I STILL managed to reduce my expenses by $23,881! (compared to a year when I did neither of those things)

So how did I do it? Good question, I was asking myself the same thing.

And it wasn’t by shopping around for a cheaper car insurance (by all means do that too if you want to, but I didn’t); and it wasn’t by cutting my gym membership or Netflix subscription… I don’t have a gym membership, and I still had Netflix in 2023 (although I have now cut it – but that’s a whole other post!)

So if those are some of the ways I DIDN’T do it, how DID I do it?

I began 2023 deciding that this was the year I was going to sort my financial sh*t out.

And I guess that was the start….

After 4 years of being single and struggling to pay my mortgage on one income, making the decision that I was actually going to do something about this struggle, not just talk about it or lose sleep over it, was the first step.

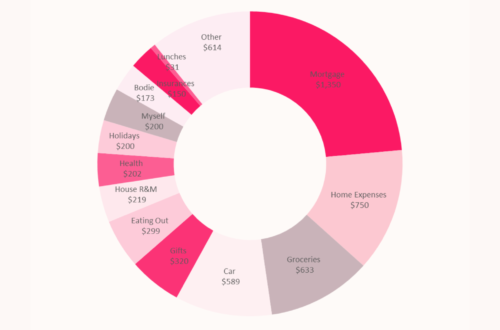

I decided that in order to actually make meaningful changes though, I first needed to know where I was starting from. So, at the beginning of January 2023 I sat down and worked out for 2022 where every single cent of my income went – and there were definitely a few surprises (such as almost $8,000 on gifts and over $8,300 on my house and garden when I could barely afford to pay my mortgage??)

Tracking my expenses wasn’t new to me, it was something I used to do when I first moved out of home.

But as I had started to earn more, met my husband and life became more comfortable, this process became unnecessary (or so I thought)

The reality is though, that just because we didn’t need credit cards to get us from payday to payday and we were able to afford our mortgage and the occasional holiday, we actually weren’t ‘good’ with money.

We weren’t saving money. We never had an emergency fund. And we definitely weren’t thinking about investing or retiring.

So, whilst we prided ourselves on not being ‘bad’ with money, we weren’t good with it either. We were the epitome of mediocre. We worked hard for our money but never thought about how we could make our money work for us.

I am not going to beat my younger self (or my ex-husband) up too badly because you don’t know what you don’t know. And I think we were doing our best with the information we had at the time.

I was taught some good money habits growing up , like that you save for what you want, avoid credit cards, and always contribute to a company pension. But I was also taught you should NEVER make a lot of money (yes really, because people that had ‘too much’ money were bad and selfish)

Anyway, my decision to restart the tracking process coincided with a visit to see my old boss and mentor and as I overshared (as I always do with her) my financial woes, she recommended a podcast – The Happy Saver. If you haven’t read Ruth’s blog or listened to her podcast (both very different so it’s worth checking out both) please do. If like me you want to sort your money sh*t out in any way, or are on any kind of path to financial freedom or want to be, she is a source of financial wisdom on her blog and inspiration on her podcast .

I binge listened to every episode of The Happy Saver over the Christmas holidays of 2022 and inspired by the stories of everyday kiwis getting their financial sh*t together I not only formulated a budget for 2023 I also resolved to make it the year I educated myself about investing and all things finance (I started the year knowing nothing and finished 2023 with over $4,000 invested in broad based index funds…. That journey is probably worthy of a post all of its own though)

I also made the decision to share my sordid spending secrets on Instagram. Yep, that’s right, every month of 2023 I published graphs and charts declaring my income and exposing my dirty money secrets – including a breakdown of my top expenses to my friends, followers and the complete strangers of Instagram. Foolhardy and downright scary (not to mention at times embarrassing – like the month my dog cost me more than my groceries!) as this might be, what it gave me was some much-needed accountability.

Knowing that I was going to share this information month after month sure made me think twice about those extra $$$s on cosmetics (I wouldn’t want people to think I was vain) or eating out (I can’t complain I am broke and then announce I spend $500 on 2 meals at restaurants) or groceries (everyone knows I live on my own, spending $200 a week to feed one had to stop!)

So, there you have it, the simple path to cutting a shit tonne of $s from my annual spend was as simple as:

1. Deciding I was going to do it

2. Knowing where my money had been going

3. Telling my money where I wanted it to go instead (otherwise known as a budget)

4. Tracking my spending each month

5. Creating accountability for this new habit – so that I couldn’t let it slide.

And it really was that simple.

The strange thing is that I didn’t feel I missed out this year. I still bought myself some new clothes and some much needed Winter shoes, I still went to England (although for the purposes of full transparency I will clarify I bought the ticket in 2022…but I still had to pay for my spending money and Bodie’s holiday in 2023), I also went on my first ever island holiday, I went out for lunches with friends, and had the occasional dinner date. My life was frugal, but I was still living. I was just spending more mindfully.

Just as it is true that you don’t know what you don’t know. It is also true that once you know it you can’t unknow it. And once I had learned about the simple path to wealth, and the shockingly simple math behind early retirement, I knew that every $ I wasn’t spending on clothes or food, was buying me some of my time back in the future. It was buying my financial freedom! And once I equated money with time (or more importantly my time) I simply couldn’t waste another $.

I still spend my money where I see value – time with friends, experiences, visiting loved ones, travelling and seeing new places. But I don’t spend money on consumer items that end up in landfill, on expensive clothes, or on the latest gadgets (I have a refurbished iPhone 11 and a 10 year old laptop… or did for 2023, but again that’s another story)

In fact I did have to replace my television this year. Much to my dismay my 11 or 12 year old non-smart, 40 inch Veon finally died. I hated that TV when my husband first brought it home because I had also always been taught “buy cheap, buy twice” and that television was the epitome of cheap. The sound wasn’t even as good as the TV it replaced.

Yet when it came time to replace it, with my new frugal mindset I couldn’t in all good conscience argue a case for a bigger television (I live in a small house with a tiny lounge), or a smart television (I barely watch tv), and the only small, non-smart TV I could find? A 40 inch Veon. And having had my old one for over a decade, I couldn’t even make the case for a better brand because clearly Veon can be as long lasting as any ‘top’ brand. I messaged my ex-husband (yes, we’re still friends) knowing the glee it would give him to hear this. My new television cost me less than $300 and I couldn’t be happier (and my ex couldn’t be rightfully smugger).

So, if it wasn’t reducing my insurances or my Netflix subscription, how did I cut my expenses by $23,881?

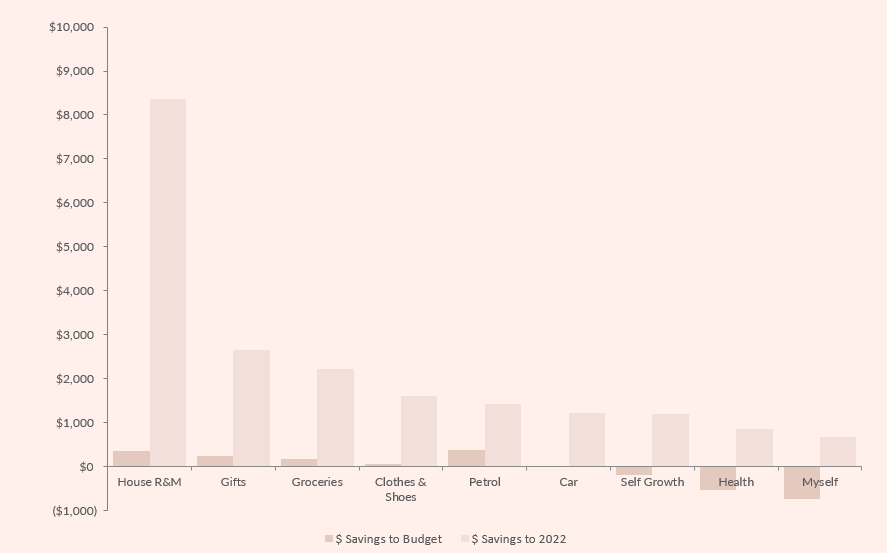

House R&M

Over $8000 came from not spending on my home. In 2022 my Mum came to visit me from England and it was the first time I had seen her in 5 years so I spent a small fortune on getting my house and garden looking nice: lawning a car parking space in my back garden, buying linen and towels for the spare room… but I can’t blame my Mum’s visit for all of my extravagance. I was a sucker for Kmart and Briscoes sales, buying things I didn’t need – I simply can’t walk past a cute mug! But all of that stopped in 2023 (well almost all of it – I bought 6 gorgeous mugs for $30 from Nood) and I saved $8,365 – despite still paying someone to do my lawns.

Gifts

I spent $2,657 less on gifts. Gifts are my love language (pom, can’t use words) but I recognised that I simply couldn’t afford to keep doing it. I also realised if I couldn’t afford to be extravagant chances are the people I was buying for couldn’t either. And it was suggested to me that my over generous gifts may actually be something that made people feel uncomfortable rather than loved. In 2023 I made an effort to spend less and for 2024 I have set myself the challenge of finding alternative ways of showing my love (since I still spent $5,262 and I don’t have a husband or any children)

Groceries

I saved $2,210 on groceries – and that is despite the cost of food being craaazy this year ($15 for a punnet of grapes before Christmas?!?!? What the actual…) Granted that last year I would have spent more than usual when my Mum was here – I wanted to spoil her with yummy local Hawkes Bay produce and treats. But I am also vegetarian, and where as I used to buy and cook a lot of meat substitutes like Quorn, this year I switched to lentils – packed with protein and considerably cheaper – to reduce my costs. And I would say I still eat well, very well in fact, spending on average $150 a week – although that also includes treats for Bodie, and the occasional skincare/beauty product. I can’t help but think that $150 is a lot for a single woman… but food is one of life’s pleasures! And I can’t resist fresh berries in the summer and the occasional pack of facon!

Clothes & Shoes

I spent $1,608 less on clothes and shoes… I can’t in all honesty think what I bought in 2022 to have been able to save that much. But I know when I first pulled together my 2022 expenses it was a shock. Although it turned out some of those $s were spent on cosmetics (because I forgot to create a separate category for that) and I have definitely made a few small changes to my cosmetic purchases this year to save myself money – buying more budget friendly creams, cleansers, and haircare; but not $1700. So the majority of that saving came from just being a little more mindful.

I never used to spend a lot on any one item of clothing, but I did tend to buy things in the sale and justify my purchases with girl math “I saved $X” instead of thinking “I spent $X when I didn’t really need to!” In 2023 I bought a small number of key, timeless pieces – a couple winter coats, a pair of linen trousers for summer, some skirts for work.

The Rest

By getting a job closer to home I have spent $1,423 less on petrol in 2023 and $1,218 less on car maintenance, so that was definitely an added bonus of my lovely new job. I also saved $1200 on self-growth. Yes, self-growth. Alongside travelling I believe spending money on yourself is the best investment you can make. It’s not selfish or frivolous, it’s important work that benefits everyone. The saving was from cancelling a monthly membership fee for UFYB. Kara Lowentheil is amaaazing but the USD to NZD exchange rate was horrific, so I sadly cancelled despite loving her work and not begrudging her a single $. If I had the money I would join again in a heartbeat because the benefits of what she teaches are priceless.

And last but not least I spent $671 less on myself. This is things like beauty treatments like getting my braz done (I don’t miss that) and facials (I do miss them!)

The only category I spent more on than in 2022 – that I had any control over (rates and insurances all went up, as they always do!) – was holidays and trips away. I am ok with that. I hadn’t travelled outside of New Zealand in 10 years, I hadn’t gone home in 11 years and I value experiences and visiting places.

You might have noticed on the chart that a few of those categories were over budget even if they were under my 2022 spending. So whilst I am celebrating the $23,881 less I spent this year, clearly I thought I could have done even better in a few areas….

What next for 2024??….

Part of me wonders how much more I could trim from my expenses…

But with my mortgage due to increase by $500 a month (based on current interest rates) and insurances and rates taking that increase to $700 a month I fear the answer is not enough. Which leaves me thinking the better question for me is, how I can increase my income in 2024?

Over the last 4 years I have gone from making $25k to $100k a year. And if you had asked me 4 years ago if I could ever make that much money the answer would have been no. So who would I have to become to make… $200k this year?

Amy

XO$