Monthly Money Review: March 2024

And just like that we’ve had Easter, daylight savings has kicked in and we’re nearly in the middle of April!! (Is it just me or was Christmas only yesterday?!) Anyway, the start of another month means time for another monthly money review.

This will be my third, but just in case it’s your first here’s a quick recap: I share these updates where I publish my personal finance numbers for the whole world wide web (but mostly just my Mum at this point) to see for two reasons.

One, it serves as part of my accountability process to keep me working towards my money goals for 2024 (the other part of my accountability process being my monthly finance meetings with my brother… which I absolutely must write a post about! I have been saying that for 2 months now)

Two, as a record of my progress. Mostly for myself – I know how much things changed for me last year and I am sure this time next year I will be looking back from a different place too, but also for any of you who might be on a similar path to me for who this might be useful. I know how much it helped me along the way to see and hear the stories of people I could relate to. I especially loved the specifics about what people spent or saved, where and how much they invested and what they did to change their circumstances. Specifics helped me to implement similar changes myself, which is why I lay it all out for you to see – and ask questions if you have any 😊

With that being said, on with the review….

Well so far I would describe this year as something of a financial rollercoaster: it’s been up and down and now back up(ish) again. If January was disgraceful and February was delightful, then March was downright disappointing.

Despite going into March with a much better money mindset than I had started February with, a big bump on my financial journey came along (as they inevitably do) and set me back, and further than I would have liked because whilst I have been working on my money mindset for almost a year, I still occasionally slip into old narratives of scarcity.

In March my car developed an issue. One that I knew would probably be quite expensive (foolish me for buying a BMW…. but I do love Lady Bea) Instead of facing it head on, I stuck my head in the sand for a week and was lucky I didn’t do more damage. When I finally got Lady Bea fixed, the issue cost me $491 which at the time you would have thought was $4900 I was so upset by it. I kept telling myself I didn’t have the money, I could feel anxiety rising within me…

But that simply was not true. It was just an old thought pattern that has been hanging around for so long now that even though he causes unnecessary suffering he is also comfortably familiar and I keep going back to him (sound familiar?) The truth though is that whilst $491 hurt I did have the money because I have my emergency fund! And much as I didn’t want to dip into it, this was exactly what I have saved an emergency fund for. And this was what I had to keep reminding myself.

Before 2023 I wouldn’t have had an emergency fund and I truthfully wouldn’t have had the money to pay for the repair. I would have been looking at either paying for it on a credit card or a loan from a friend. But thanks to the changes I’ve made to my spending and saving habits over the last 15 months I had over $3500 in my emergency fund, more than enough to cover the $491 my car repairs cost.

It was a reminder that I am in a much better place than I was even 12 months ago… and of course working on my money mindset and the stories I tell myself about money is a constant thing!

Anyway, that’s enough about money mindset, let’s dive into the numbers, starting with the gap….

The Gap

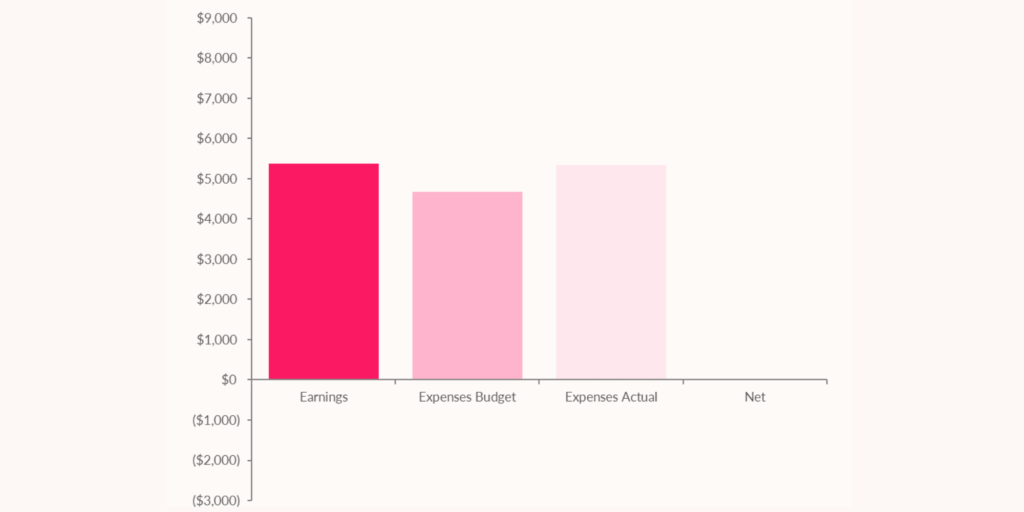

I will start with a little refresher, if you are new to either the blog or these reviews the Gap is simply the difference between what you earn and what you spend. In a business we would call it the profit, and even in our personal finances it is one of the most important indicators of financial health because you can earn a million dollars a month and still be living payday to payday if you spend $1,000,000 a month!

You may remember January’s gap was actually negative (so I spent more than I earned that month – eek) but February’s was a vast improvement at $2,871, well March’s gap was non-existent, pretty much zero (the first disappointment)

Although it wasn’t negative, so it could certainly have been worse! And I knew February was an anomaly not the start of a new trend, so I shouldn’t be as disappointed as I am… but it was really nice seeing such a healthy gap (definitely something I could get used to).

In February getting $300 from my business was a contributing factor to that healthy gap. However the lord giveth and the lord taketh away or in this instance my business does, and I actually had to top up my business account by $150 in order to cover my hosting for the month – not ideal and something I need to work on.

But worse than the non existent gap and the $150 my business cost me was how much over budget my expenses were. I had budgeted expenses of $4,671 but my actual expenses were $5,346 a difference of $675 which you don’t have to be an accountant to work out was more than the $500 car bill!

I actually think March was not a reflection of costs beyond my control, but a reflection of me feeling a bit flush after February. Sometimes it is hard to see which mindset is more damaging to my financial journey: scarcity, and how it holds me back from thinking I can make more, or abundance which for me still leads to overspending (although I suspect this stems from my thought that people who have a lot of money are selfish and unlikeable)

Expenses Breakdown

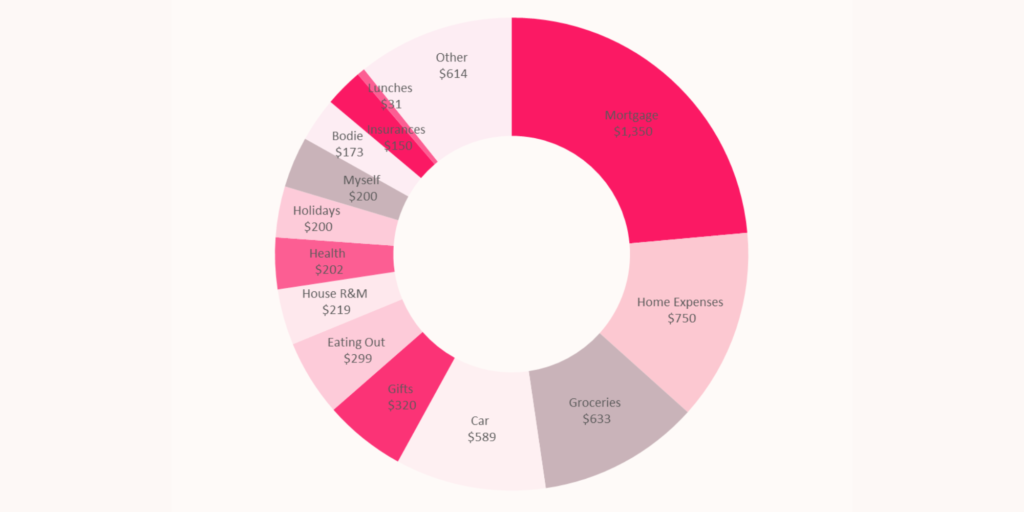

My expenses for the month were $5,346 actually pretty similar to February, but as I mentioned some $675 more than I had budgeted. If you have taken a peek at my last two monthly reviews you might notice that this month I have added $ figures to my pie chart so you can see exactly where my money went.

As is the case for most kiwis, my housing costs are by far my biggest expense. First there is my mortgage which accounted for $1,350, followed by home expenses which include house insurance, rates (which Napier City Council have informed us will be going up by another 24% next year!), internet, power (which for me living on my own is usually somewhere around $100 each month) and repairs & maintenance (which is usually just my gardener).

Groceries was $633 for the month which was $28 more than I had budgeted but not too bad. Back in 2022 before I started tracking my spending my groceries averaged $840 a month, so it’s a BIG improvement on that number – especially given how much food has gone up over the last 2 years (if I had continued spending as I had my monthly groceries would be costing me $969 based on the food CPI for the last 2 years).

Then there was my car which I have already covered, followed by Gifts. March was another big month for Gifts at $320 – $45 above budget, but I thought I might have undercooked my gifts budget for this month as it was 2 of my dearest friends birthdays AND Mother’s Day in England. And then I had forgotten to factor in Easter, which whilst it fell on April 2nd, eggs and gifts were bought in March. This is one area I really struggle with being frugal and I need to keep working on finding alternative ways to show my love – like hand written notes, baking and home made gifts.

I also spent $299 on eating out, $149 more than I budgeted for March. Some of this related to the birthdays I mentioned, which I wouldn’t change for anything, but I do need to curb my other eating out costs. Of all of the areas I could blow my budget, eating out is the one I mind the least but at the same time, if it is a choice between eating out and paying my mortgage….

I spent $200 on Holidays which I hadn’t budgeted for. But it is a girl’s weekend to Auckland in May for one of my very best friend’s 40th birthday – these are the things I will always find the money for because people only turn 40 once!

And I spent $200 on myself, which was for another ceramics class which was meant to start later this month (and I was soooo looking forward to), but after my car issue the lovely Emily has kindly agreed to refund me the money I have paid so far for the class.

I should mention, as I am always quick to state when the opposite is the case, Bodie was actually an area where I saved last month. I had allowed $100 in my budget (for a hair cut I think) and he actually cost me nothing (because I include his treats in my groceries), so I guess he can stay for another month.

Investments

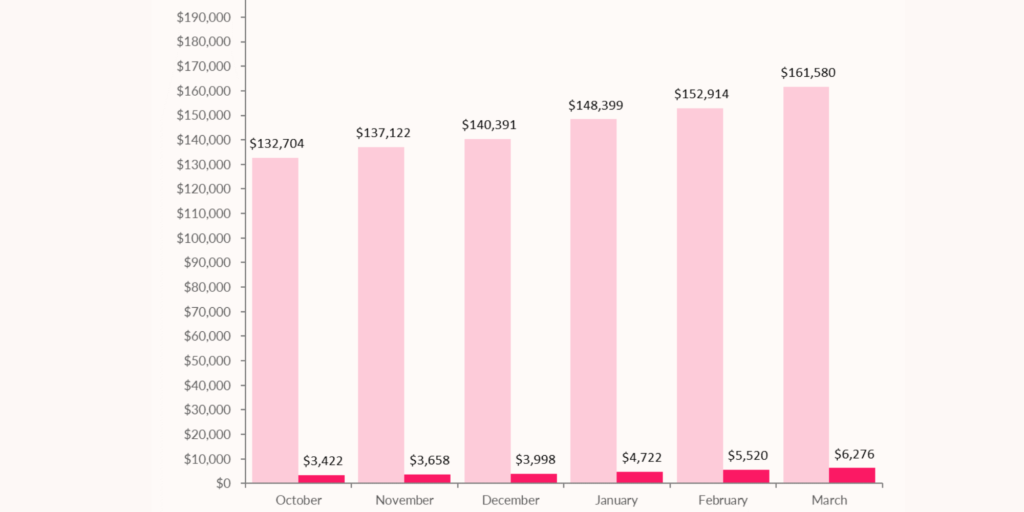

My investments were my one bright spot in the otherwise disappointing March! It was another great month for both my Kiwisaver and my Sharesies account which is my 2 forms of investment at the moment. My Kiwisaver took a massive leap (it’s now $21k up on where I started the year) and I smashed the $6k milestone in my Sharesies (with returns hitting the $2,000 milestone) All of this is being driven by the outstanding performance by the S&P 500 and in particular Nvidia…. which still makes me nervous.

Investments Breakdown

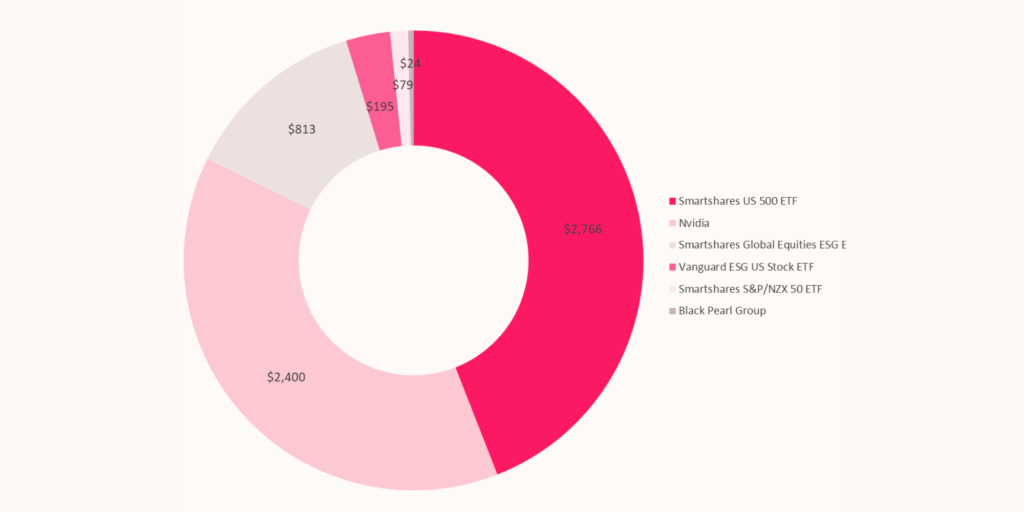

In case you’re interested here is exactly what that $6,276 in Sharesies is made up of …

I invest $100 the day after every payday and I get paid fortnightly. But in March I invested $300 because there were 3 pays in February and the investment for the last one fell on the 1st of March. Of my investments 80% continues to go to the US 500 ETF and the remaining 20% to Nvidia. The other shares I hold are leftover from early dabbling days. At some point I might sell them and simplify my investments, or I might dabble some more as I am still learning.

So what about April?

Once I have reviewed the prior month I look ahead to the current month not necessarily changing my budget (I’m an accountant so for me once a budget is set….) but changing my spending habits if I know something is coming up that I didn’t budget for.

In April I had budgeted my expenses to be significantly higher, in fact I had budgeted it to be $1,761 higher than my income (which is some seriously dodgy budgeting right there!) I did it because I was hoping to be booking a holiday for later in the year. But the reality is I don’t have the savings I thought I would have when I created this budget, so it relies on me getting some income from my business (because I will not dip into my emergency fund for a holiday) and at the moment that looks doubtful (disappointment number 2)

Last month I had hoped to be able to replace that front tyre on Lady Bea that I know needs replacing, but as it didn’t happen in March it will definitely need to happen in April.

My focus continues to need to be on finding ways to make additional income. I have budgeted for an $300 of Other Income (i.e. not from my base salary), but if I want to book that holiday I need it to be 10x that amount. My boss had suggested there could be some additional hours for me, but I doubt it will be this month. I have a Pinterest course that I am currently not marketing… and I want to start working with women on their finances, so that’s two ways I can think of that I might be able to start generating income with. The problem is I need to stop thinking and start doing!

Well I am going to sign off for another month but as always feel free to leave questions and feedback – is this helpful? Would you like to see anything else included (or excluded) each month?

Amy

XO$

You May Also Like

Monthly Personal Finance Meetings Are More Exciting Than The Latest Season of Bridgerton!*

Was My House My Worst Investment??