Monthly Review: January 2024

Part of setting financial goals – or at least achieving them – is having accountability.

A process by which you hold yourself accountable for doing what you say you are going to do.

I have 2.

Firstly my monthly money meeting with my brother. I put him on the path to FI when I bought him The Simple Path to Wealth by JL Collins (if you haven’t read it, it really is a life changer) for his birthday last year. Now that we’re on this financial journey together we meet on the first Wednesday of every month to go through our spreadsheets – and generally have a good gossip. It’s such fun, it’s something I look forward to every month 😊

(although he usually does it at the crack of dawn on his day off, so he might disagree)

Ben and I hadn’t Skyped (he lives in the UK) for probably the best part of a year before we started these monthly money ‘meetings’. I love that our shared goal and interest in personal finances and all things investing has given us something to talk about and brought us closer together again.

That’s not what I am sharing on the blog today though (Ben will be relieved to hear)

My other accountability process is publishing my numbers for the world to see.

I originally started doing this on my personal Instagram profile (and I may continue to do that) but now I have this blog I thought it was the perfect place to dissect and divulge how disgraceful or delightful my month financially has been.

Whilst the numbers are all about what’s happened, they inform my decisions and next steps for the following month. So it’s an important part of achieving those money goals I set for 2024.

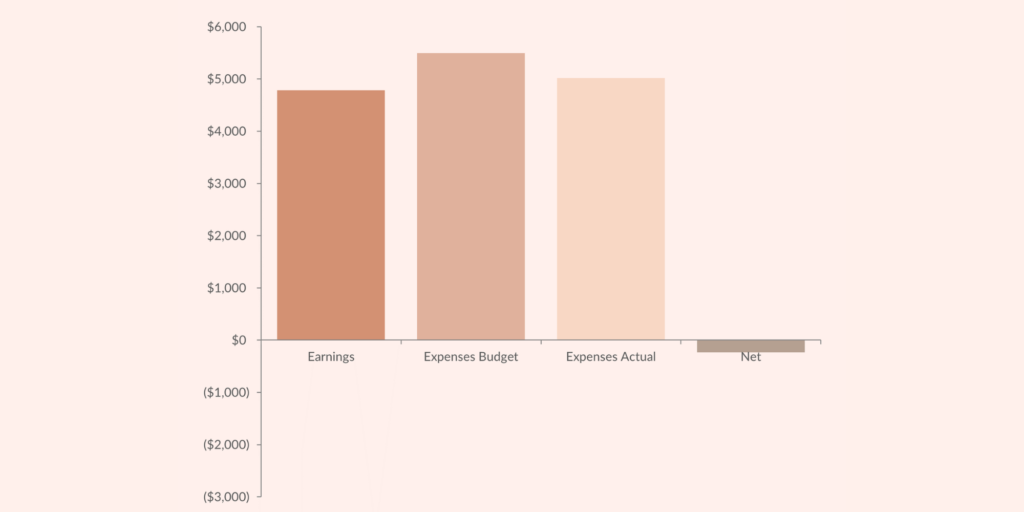

The Gap

First of all, what is The Gap? Well it’s the difference between what you earn and what you spend – in a business we would call it the profit. And the Gap is an important number because it is an indicator of your financial health (just as it is in business)

It doesn’t take an accountant to know that if you earn significantly more than you spend, then you are probably looking pretty healthy financially.

Unfortunately as you will see that’s not how I started my year….

My income for the month was $4,785 and my expenses for the month $5,019 which gives me a negative gap of $234…. I was going to say that wasn’t the start to the year I was hoping for, but actually I had budgeted for my expense to be even higher, more like $5,496, so the result was better than I expected!

Why was I budgeting to spend more than I earn? Because I knew I had some commitments, celebrations, and expenses such as going to Auckland with my friends, my Mum’s 70th birthday and my car needing work to pass its WOF. Despite this negative gap I still invested in Sharesies and to my Emergency Fund because I prioritise these 2 things over everything else.

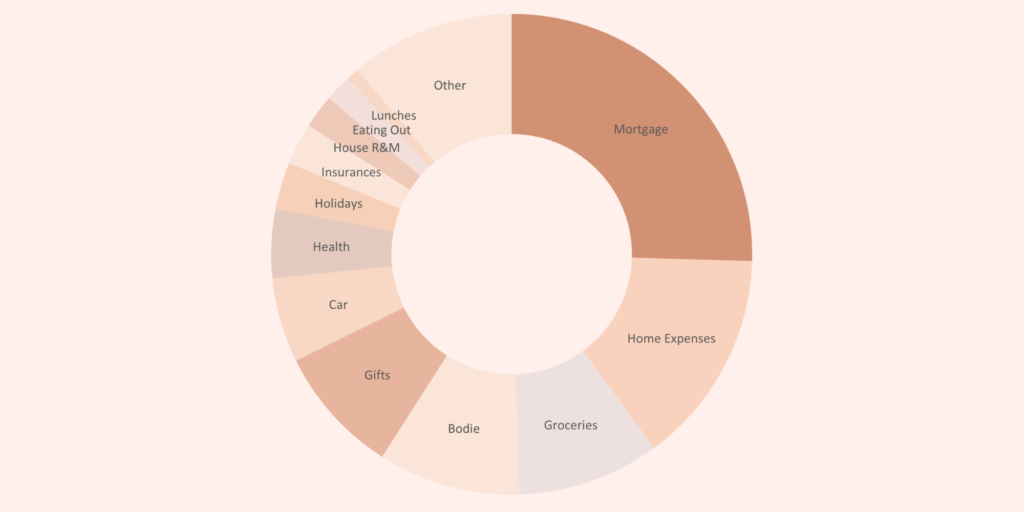

Expenses Breakdown

So where did I spend that $5,019?

Well a good quarter of it, $1,350 to be exact, went on my mortgage (and that number is going to rise significantly in October when my whole mortgage rolls of its current fixed term)

Home Expenses was my next biggest expense at $766 which include rates and insurance (both of which have gone up significantly this year), internet and power. I am a low power user as it’s just me, and Bodie of course, and I try to keep my electricity usage to a minimum by using my stove top rather than my oven, open windows rather than put on the air con, turn out lights when not in the room oh and of course there’s the fact I have challenged myself to NO TV in 2024!

Groceries were next and I probably over budgeted here, but with a birthday and the holidays in January I thought I might spend more than I actually did, so this was one of the areas I saved against budget. I spent $508 in January which averages $127 a week, against a budget of $214 a week, which seems high but was based on last year.

Bodie on the other hand was NOT an area I saved! (it’s a good thing he’s cute as I always say) January was an expensive month at $507 because it included two trips to the kennels, a visit to the groomers and the vets for a grass seed, as well as his usual insurance. And that doesn’t include treats as I pay for them in my groceries! No doubt about it, pets are EXPENSIVE!! So if you can’t afford to pay $300 a month please don’t get one.

Gifts was just over $450 of the $5,019 I spent in January. It actually could have been higher but I paid for some birthday presents in December. I am trying to reduce my spend on gifts this year and find alternative ways of showing my love… but when you’re on the other side of the world and it’s your Mum’s 70th birthday…. I wish I had spent more!

My car was another area I managed to save against budget in January because not going anywhere over the holidays meant that I didn’t have to refuel my car once in January! It was still an expensive month compared to normal though because of the repairs that needed to be done.

I spent $245 on my health, which seems like a lot for someone who is as ridiculously well and healthy as I am. But this was purely on my private health insurance and chiropractor visits – so it’s maintenance rather than repairs.

Nearly $200 was spent on holidays and that actually wasn’t budgeted for. It was just the cost of the trip to Auckland and as one of my goals is a mini adventure each month and one of my values is friendship and connection, I would gladly have spent twice as much.

The rest probably isn’t worth commenting on as we’re getting to such small amounts – although as you can see they all add up!

Overall I would say I wasn’t unhappy with my spend in January. Most of it was pretty much where I expected it to be with just a couple of surprises. But I was able to adjust my spending elsewhere to minimise the effect of those surprises – something that is only possible when you have good control of your spending via a budget and tracker.

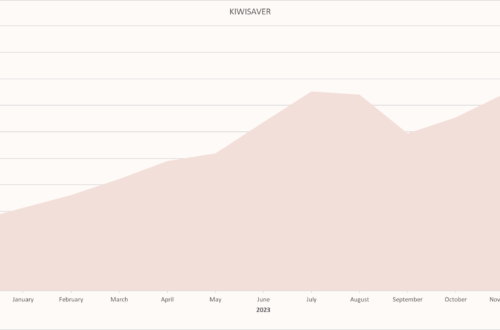

Investments

This is a new chart for this year and just shows the 6 month trend of my investments in Kiwisaver and Sharesies. As you can see both are going in the right direction, after a slight blip in my Kiwisaver in September. The truth is though that I know these numbers will be massively volatile, so sometimes I worry about including them in my net worth because I don’t want to feel poorer when they inevitably go down.

But the only price that matters when it comes to shares is the price you buy them at and the price you sell them at. As I can’t touch Kiwisaver for another 20 years and I have no intention of selling my shares their value really doesn’t matter at this point. I only track them as a learning exercise.

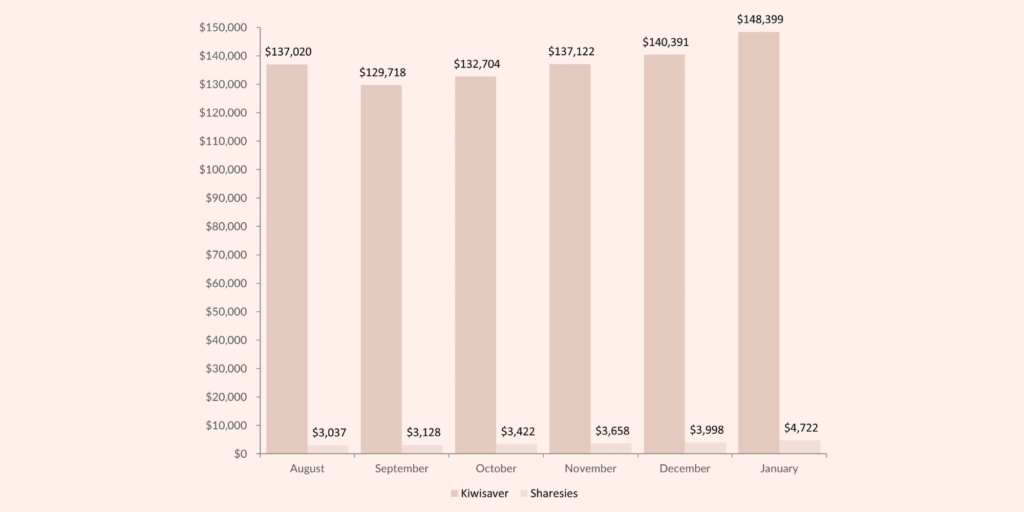

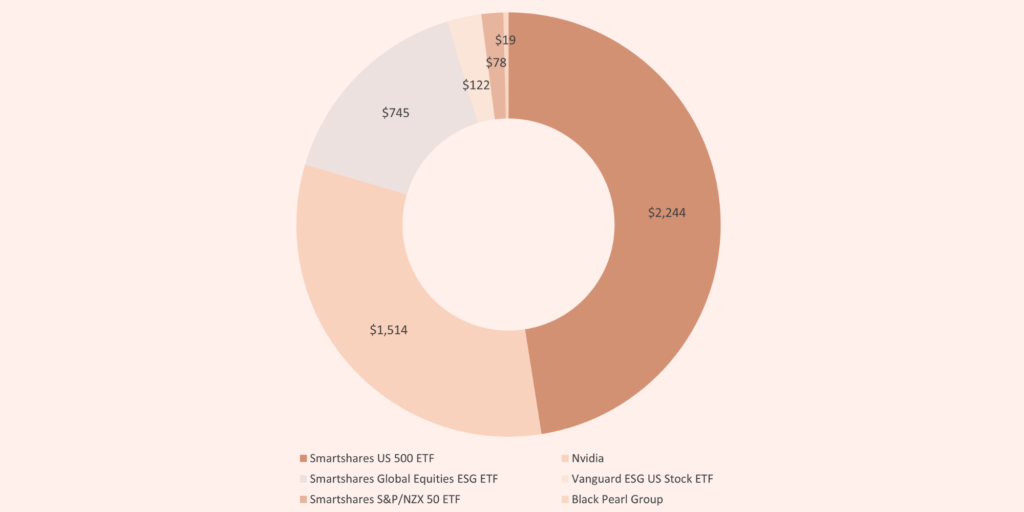

Investments Breakdown

Just in case you’re interested here is exactly what that $4,722 in Sharesies is made up of …

I invest $100 every payday and I get paid fortnightly, so in January I invested $200. Of my investments 80% goes to the US 500 ETF and the remaining 20% currently goes to Nvidia which is an individual company that has been on quite the run – my return on this investment is around the 60% mark at this point. I keep waiting for it to go down, but instead it just keeps going up thanks to AI.

I wonder if I should research how to identify a bubble? First there was the dot.com bubble, then the housing bubble, is AI next??

What does this all mean for February?

Once I have reviewed January I take a look at February in light of what I know. Not necessarily changing my budget (personally I am of the ‘a budget is a budget’ mindset, but you do you) but changing my spending habits if I know something is coming up that I didn’t budget for.

For example, I know that Bodie’s food which I budgeted for in January came out of my bank on the 1st of February. Which means I will need to try to keep my groceries under the $636 I budgeted.

I might also reduce my eating out spend which I originally budgeted $150 – what with Valentines Day and everything! But the joy of being single means I can probably save that.

More importantly I want to increase my income in February. I am going to do this by offering bookkeeping services to small businesses at the weekend. This will be very ad hoc work, so not a regular income I can rely on, but every little bit helps and with year end coming up I figured it’s a good time to do it.

Well I am going to sign off for January but let me know if this was helpful or if you would like to see anything else included (or excluded) for February.

Amy

XO$